Ideas for a Better World newsletter

Is AI a Race to Zero?

The AI pricing model is a ticking time bomb. As tokens follow the path of the SMS, we’re witnessing a race to zero that will force foundation models to evolve or become mere pipes.

The companies building the most powerful technology in history may be building themselves out of a business. We've seen this before.

Twenty-five years ago, your mobile bill was an itemised list of constraint. Calls were charged by the minute. Texts were charged individually. Data came in bundles,.many of us will still remember, 500MB, 1GB, and when you ran out, it sucked. The telcos had built a business on scarcity. Not real scarcity, exactly. The cost of carrying one more minute of voice across a network already running was close to nothing. But metered pricing was the model, and it worked, right up until it didn't.

WhatsApp made SMS a rounding error. VoIP ate into the call. Unlimited data plans killed the bundle. The pipes endured. The pricing model did not. BT, Vodafone, AT&T became infrastructure businesses, solid, necessary, and almost entirely unable to capture the value that flowed through them. The surplus migrated upward, to the platforms and applications built on top.

The telcos built the road. Someone else built everything worth going to.

I've been thinking about this a lot in the context of AI.

Tokens are the new SMS

Right now, the major AI companies price on tokens. Input tokens, output tokens, context windows. It is a metered model applied to a unit that is getting exponentially cheaper. A year ago, running a complex query through a frontier model cost roughly 100 times what it costs today. The trend line is not flattening.

Open source is accelerating this. DeepSeek demonstrated that a model approaching frontier capability could be built and run at a fraction of the anticipated cost. Llama, Mistral, and others are narrowing the gap between open and closed models faster than most people predicted. When the model is free, the token is free. The meter breaks.

The cloud providers are doing the rest. AWS, Azure, Google, commoditising inference the same way they commoditised compute. Abstract the model, price it down, make it interchangeable. If you can swap one foundation model for another with a single line of code, none of them can hold margin at the infrastructure layer for long.

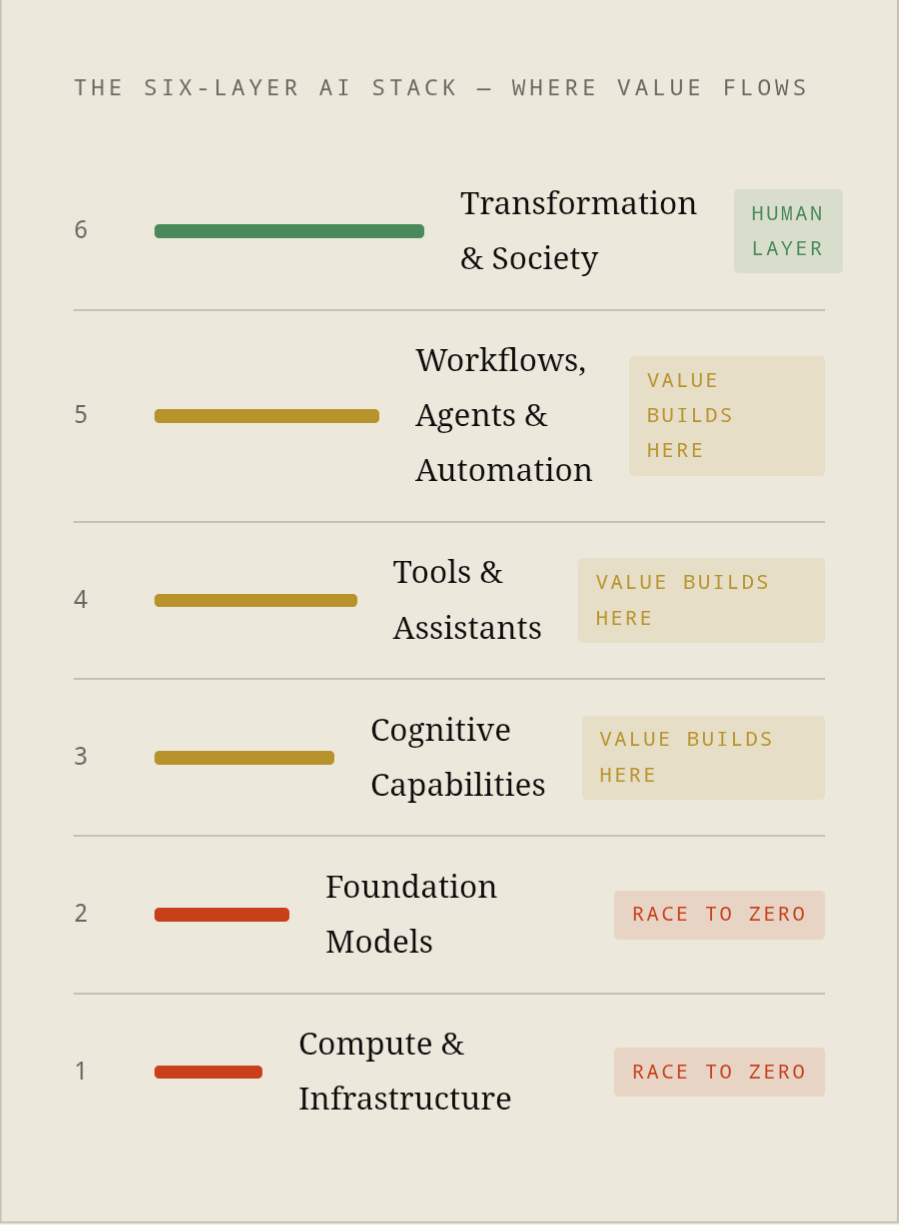

In a piece I wrote a few months ago — AI: Everything, Everywhere, All at Once — I mapped AI as a six-layer stack — from compute and infrastructure at the base, through foundation models, cognitive capabilities, tools and assistants, workflows and agents, up to transformation and society at the top. The race to zero is a story about layers one and two. The interesting value question is about everything above them.

The energy question

There is one argument that genuinely distinguishes AI from the telco era, and it deserves its own dedicated piece, which we will return to. For now, the short version.

Training and running large models is extraordinarily power-hungry. This is a physical constraint, not a commercial one. The telcos never had to build power stations. Small modular reactors are moving from concept to deployment. Nuclear fusion is edging toward viability. The trajectory of energy costs for AI infrastructure, like the trajectory of compute costs before it, points in one direction. When abundant, near-zero marginal cost energy arrives, the last structural cost barrier for inference collapses with it.

The full implications of that, for AI economics, for geopolitics, for who controls the infrastructure of intelligence, warrant more space than we have here. We'll come back to it. For now: energy is a speed bump, not a wall.

The race to zero has a shape

This is not a cliff. It is a slope, and the gradient matters.

Capital concentration means the floor doesn't fall out overnight. The compute required to stay at the frontier may produce a global oligopoly of three or four players, organisations that can sustain the infrastructure investment long enough to convert model leadership into something more durable. The telco transition took the better part of two decades. AI commoditisation will move faster, but the labs with the deepest pockets have a runway. What they build on that runway is the only question worth asking.

The data moat is real, but it is a clock, not a wall. Two years of ChatGPT usage data, clinical query patterns built into a healthcare deployment, engineering workflows embedded into a procurement system, none of that is replicable by an open source release. But it has a half-life. The advantage compounds only as long as it keeps converting into something stickier: embedded relationships, fine-tuned domain models, workflows where the underlying model becomes invisible. The labs that make that conversion survive commoditisation of the model itself. The ones that don't are left holding an expensive pipe.

The market also splits in ways that determine the speed of the slope. Consumer AI commoditises fast, switching costs are low, price sensitivity is high, and the race to zero plays out in plain sight. Enterprise AI is different. Workflow integration, compliance requirements, domain-specific fine-tuning — these create friction that slows the transition significantly. The companies that read this early and weight toward deep enterprise embedding rather than consumer volume are already positioning themselves above the layer where the race to zero actually happens.

The race is real. The timeline gives you a window. What you build inside that window is everything.

The part the telco story gets exactly right

The direction of travel is clear. The model layer is becoming infrastructure and with that comes the logic of infrastructure economics.

That means regulation. The telcos didn't just commoditise. They became utilities. Rate-setting, access requirements, interoperability mandate. These were both cause and consequence of their loss of pricing power. The EU AI Act, emerging US frameworks, calls for model auditing and mandatory disclosure: these are the early signals of a regulatory logic that, if it follows the telco pattern, will eventually treat foundation models as public interest infrastructure. That is not a fringe view. It is where the policy conversation is heading.

If that happens, the pipe analogy is complete.

The vertical integration trap

Here is where the telco analogy adds something its authors didn't intend.

Recently, OpenAI acquired TBPN, a tech industry talk show with a loyal and credible audience. The strategic logic is clear enough, to own the distribution layer, not rent it. Build a trusted channel that sits inside your organisation. The a16z media playbook, taken one step further.

"They've killed their brand in exchange for some OpenAI shares. Who is going to tune into a show about tech which will inevitably talk a great deal about AI, when it's literally owned by one of the major AI players?"

Mike Butcher, Founder, Pathfounders

He's right, and the principle extends well beyond media. The moment you own the channel, you destroy the trust that made it worth owning. This is not just an editorial independence problem. It is a structural warning about what happens when platform players try to own everything above the infrastructure layer.

Google learned this. Its AI overviews began absorbing answers directly in search results, disintermediating the publishers and businesses that had built on top of Google's platform. The backlash was immediate, from publishers, from regulators, from advertisers. Google wound back the approach. The lesson was uncomfortable but clear: you cannot simultaneously be the platform other people build on and the entity that captures all the value those people create. The trust relationship with the ecosystem collapses. You have to leave space for your customers in the process.

OpenAI is walking the same path. API business on one side, ChatGPT products on the other, media acquisitions on top of that. Each move makes the platform less safe to build on. Every developer who relies on OpenAI's API is also, now, competing with OpenAI's own product ambitions. That tension does not resolve. It accumulates.

The telcos tried vertical integration too. The AOL Time Warner mergerpipe is one of the most studied failures in corporate history. Owning the road and the destination turned out to be harder than it looked. The logic was sound. The execution was catastrophic. And the underlying problem was not operational. It was structural.

Neutrality is the asset. Ownership destroys it.

So where does the value end up?

The telco era produced the most valuable companies in history. Almost none of them were telcos. The value didn't disappear, it moved. Google, Apple, Amazon built on top of infrastructure they didn't own and captured surplus the infrastructure providers couldn't hold.

The same migration is beginning now. Vertical AI companies building for specific industries, clinical, legal, engineering, financial, where proprietary data and domain expertise create positions the general models cannot replicate. Agentic platforms orchestrating multiple models across complex workflows, where the value is the orchestration, not the underlying inference. Companies embedding AI deeply enough into operations that the model becomes invisible and the switching cost becomes existential.

As I argued in that earlier piece, the most interesting companies in AI are not the ones operating at a single layer of the stack. They are the ones connecting multiple layers, reaching down into capabilities while extending up into workflows and decisions. That is where the surplus is accumulating. Not at the token level. Not at the model level. At the intersection.

None of these companies are making headlines yet. That is precisely the point.

Is AI a race to zero?

For tokens, almost certainly yes. For the companies that figure out what sits above the token, probably not.

The uncomfortable truth is that the firms currently valued most highly in AI may be building the most important infrastructure of the century while inadvertently pricing themselves toward the economics of a utility, and then compounding the problem by trying to own the layers above them, which poisons the ecosystem they depend on.

The telcos built the road. They then tried to build the city too. It didn't work then. There is no particular reason to think it will work now.

Someone else will build everything worth going to.

The question worth asking is: are you building on the right layer?

Until next time,

Editor, Ideas for a Better World